Download

Prior to the 2003 regime change no private sector gas projects had been implemented in Iraq and gas prices were heavily subsidized, both nationally and in a regional context**.

However, since 2007, two major gas projects have been signed, the first in Kurdistan by the Ministry of Natural Resources (MNR) and the second in Basra province by the Ministry of Oil (MoO). In addition the MoO has signed service contracts for three gas fields.

Each of these projects has been structured under different commercial terms, resulting in different gas price mechanisms.

However, the Iraqi government has contracted Booz & Company to develop the Iraq National Energy Strategy (INES), the executive summary of which was recently published in MEES (14 and 21 June). INES contains recommendations on gas pricing.

Furthermore, the World Bank is working on another pricing mechanism for associated gas in Iraq. The details of these proposals to establish a unified federal framework for gas pricing are yet to be made available. Moreover, much will depend on the locality of these projects and the fiscal regime adopted. The following is a brief outline of the shareholding of gas development projects in Iraq which will influence gas pricing policy for domestic consumption and exports:

1. Kurdistan region development of Khor Mor and Chemchemal gas fields***

-

•Service contract signed with the MNR (direct negotiation).

-

•Shareholders: 80% Dana Gas and Crescent Petroleum (JV), 10% MOL and 10% OMV.

-

•Current gas production 340mn cfd of feed gas for power generation.

-

· •Current liquid production 15,000 b/d of condensate.

2. Basra Gas Company (BGC) gathering and development of associated gas**** from Rumaila, Zubair, West Qurna and possibly Majnoon fields.

-

Service contract signed with the MoO (direct negotiation).

-

Shareholders: 51% South Gas Company, 44% Shell and 5% Mitsubishi.

-

Current gas production 350-400mn cfd (feed gas).

-

Potential production of 2-4bn cfd.

3. Iranian gas supply to Iraq by pipeline^ for electricity generation.

-

Agreement between the Iraqi Ministry of Electricity (MoE) and the Iranian MoO

-

Iran to supply Iraq with approximately 850mn cfd of dry gas.

-

Gas sales agreement based on international market.

-

A 56-inch pipeline from Iran to Iraqi midland provinces estimated to cost $365mn.

-

Pipeline could be extended to Syria and Lebanon.

4. Non-associated gas fields, third licensing round. Service contracts signed with the MoO (see Table 1).

Joint Venture Companies

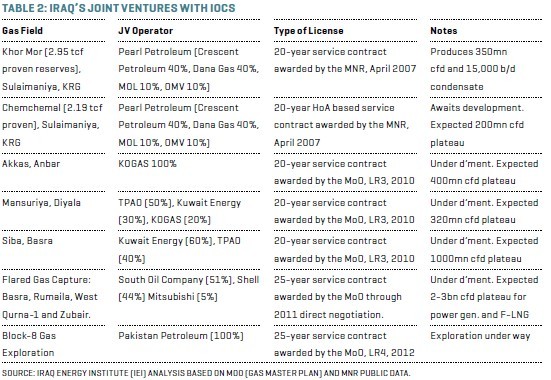

Since 2007, both the federal MoO and the KRG’s MNR have signed various long-term contracts through bid rounds and have entered into direct negotiations to form joint ventures (JVs) with IOCs. Table 2 outlines in chronological order the formation and structure of each JV.

Analysis of Gas Pricing Scenarios

Basra Gas Company

The economic model of the project was drawn up with the objective of maximizing benefits to Iraq while at the same time providing an acceptable return for the foreign partners. The gas pricing mechanism calculates the dry gas price based on a direct derivative of high sulfur fuel oil (HSFO), which is itself based on the crude oil price^^. The raw gas price is a backward calculation from the dry gas price utilizing a very large and detailed set of formulas. The CIT rate is 35% and the Internal Rate of Return (IRR) of the project is set at around 15%. In the event the IRR exceeds this figure, the price of raw gas will be raised to increase SGC’s share in the revenue and reduce BGC’s IRR.

The formula for dry gas price calculation reads:

[Crude oil price/tonne converted to HSFO price/tonne] X [Reduction factor] / [Heating value of 1 tonne HSFO]

Hence, based on different crude oil prices of:

>$75, dry gas price is $3.22/mn BTU, and

>$100, dry gas price is $4.29/mn BTU, and

>$110, dry gas price is $4.72/mn BTU.

By comparison, elsewhere in the Middle East gas is currently sold at around $2.0-2.5/mn BTU at the current crude oil price of about $85/B.

As for the raw gas price for BGC, it is determined by a number of factors (such as IRR and windfall) introduced in a long series of equations^^^.

However, gas pricing elsewhere in Iraq may pose a serious challenge, since dry gas is priced as low as $0.60/mn BTU for the fertilizer industry and at not more than $1.20/mn BTU for electricity generation and other industries. Low domestic gas prices due to the heavy subsidy imposed by the government on BGC do not offer sufficient value to underpin the investment required.

Instead BGC must rely on the returns it can generate from the higher value of NGL (condensate and LPG) extracted from the raw gas and on a set of formulas, linked to the price of fuel oil that determines the net price SGC pays for gas processed by BGC.

Although BGC does not itself market any gas within Iraq, it obviously remains dependent on how quickly demand develops, particularly for gas fired power generation, petrochemicals, fertilizers and heavy industries where gas is the primary feedstock.

Iranian Gas Deal Scenario

The Iranian gas agreement with Iraq is rather ambiguous as a result of conflicting statements by senior Iranian officials and the scant information revealed by the Iraqi authorities.

The contract signed by the Iraqi MoE and the Iranian MoO is for 850mn cfd for 4 years^^^^. The price of the gas has not been announced, but is said to be at “world market prices,” whatever that means.

The Iranian Minister of Petroleum stated that the agreement with Iraq would provide the Iranian treasury with a daily minimum of $10mn. That would suggest an export gas price of around $11.76/mn BTU.

Furthermore, the 56-inch pipeline that is being constructed for that deal would appear not to be for the 850mn cfd deal alone.

Iran has plans to expand exports to Iraq in the future as well as exports through Iraq to Syria, Jordan and Lebanon, and an earlier statement from the Iranian Ministry of Petroleum claimed that 1,600mn cfd would eventually be transported through the pipeline.

International Recommendations

Due to inherited practices and laws, Iraq’s gas market requires serious policy reforms before a viable price mechanism can be defined.

The federal government needs to work out a plan to phase out subsidies and make the local gas market competitive, while improving the country’s ability to attract foreign investors for international trades. Table 3 shows the netbacks of exports to selected regional and international markets^^^^^.

As for the IEA’s Iraq Energy Outlook, this assumes that dry gas costs are low, since production in Iraq is generally accompanied by substantial output of natural gas liquids, while supply costs for individual projects could vary significantly.

The gas feedstock is assumed to be non-associated, with the exception of southern production feeding into a possible LNG plant, which is assumed to be associated gas.

In this IEA scenario, production costs do not include taxes or royalties, and the cost of shipping LNG to the Asia Pacific market is an average of the cost of transportation to the Indian and Chinese markets. The bulk of the cost, in any case, consists of the cost of facilities for LNG liquefaction, and import price assumptions for 2020 are from the IEA central scenario.

Comment here